Full Text

Introduction

Medical tourism is recognized as an industry and it offers tremendous potential for the developing countries like India because of their low-cost and high hospitality advantage. The industry has the potential to show the same exponential growth that the software and pharmaceutical industries have shown in the last decade. Medical tourism is likely to be the next major foreign exchange earner for India due to an increasing number of foreign patients. Medical tourism, which is considered to be the next driver for Indian healthcare growth, is perceived as one of the fastest growing segments in marketing ‘Destination India’ today. India with advanced medical services coupled with compassion has become a haven for medical tourists.

India is considered as the leading country promoting medical tourism and now it is moving into a new area of "medical outsourcing," where subcontractors provide services to the overburdened medical care systems in western countries. The main reason for India’s emergence as a preferred destination is the inherent advantage of its healthcare facilities. Today Indian healthcare is perceived to be on par with global standards. Some of the top Indian hospitals and doctors have strong international reputation. But the most important factor that drives medical tourism to India is its low cost advantage and courteous services.

These factors will enable the domestic and global medical technology companies to understand the emerging business opportunities and the healthcare system in India. Further, this will help major companies to understand the Indian capabilities for making investments in India in this sector, which in turn would contribute to the economic development of the country.

Medical tourism is alternatively called health tourism or wellness tourism. It is a term that has risen from the rapid growth of an industry where people from all around the world are travelling to other countries to obtain medical, dental, and surgical care while at the same time touring, vacationing, and fully experiencing the attractions of the countries that they are visiting. It is a silent revolution that has been sweeping the healthcare landscape of India for almost a decade. With countries like India, Mexico, Singapore, Brazil, Argentina, Greece, Costa Rica, Dominican Republic, Peru, Hungary, Israel, Jordan, Lithuania, Malaysia, South Africa, Thailand and the Philippines actively promoting it, its future is sure to be bright. The domestic medical industry in India is trying all out to grab its pie from the evolving global health bazaar.

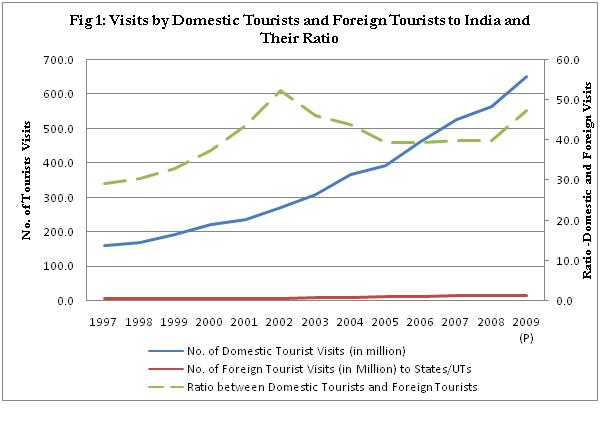

Medical tourism is a service with which a greatly lucrative potential is attached. Medical tourists are generally residents of the industrialized nations of the world and primarily come from The United States, Canada, Great Britain, Western Europe, Australia, and the Middle East. But more and more, people from many other countries of the world are seeking out places where they can both enjoy a vacation and obtain medical treatment at a reasonable price. The visit by domestic tourists and foreign tourists to India and their ratio has been shown in Figure. In the near feature, it will become a major driver of the Indian economy along with information technology, biotechnology, and technology enabled consumer services. With the international media constantly telecasting scenes of foreign people getting knees replaced, hips resurfaced, and dental works done here at throw-away prices, that too in the ambience of a five star resort, the demand from the nationals of Western Europe and the US for medical treatment in India is ever increasing. Now, companies that help arrange such travel are eying a far bigger market: U.S. and western European employers who want to save money on their health care costs are showing interest in this regard. Apart from being prohibitively expensive, it is the waiting time for treatment/ operations, (often ranging from six months to a couple of years or even more) which motivates people to travel to countries like India for medical treatment. Also, health insurance schemes do not often cover elective treatments like cosmetic surgery and hence there exists high inclination for people from the rich industrialist countries to travel abroad for the same. In fact, very shortly the health care insurance companies themselves encourage medical tourism as a potential cost-saving measure.

Figure 1: Visit by domestic tourists and foreign tourists to India and their ratio.

Figure 1: Visit by domestic tourists and foreign tourists to India and their ratio.

Hospitals in the developing countries that enjoy cost leadership have added flavor to this desire by packaging everything, ranging from medical treatment, travel and hospitality services, to local-sightseeing within an all-inclusive offer. With the distinction between hospitals and hospitality establishments increasingly being narrowed down, medical tourism will get a shot in the arm. With India reaching nearer to the status of a global healthcare destination, the revolution is not restricted to elitist hospitals; a range of alternative healthcare services providers like ayurvedic, naturopathic, homeopathic, and yogic establishments too benefit from the big wave.

Medical tourism in India

According to the Confederation of Indian Industries (CII), India is unique as it offers holistic medicinal services. With yoga, meditation, ayurveda, allopathy, and other systems of medicines, India offers a unique basket of services to an individual that is difficult to match by other countries, says CII. Also, clinical outcomes in India are at par with the world’s best centers, besides having internationally qualified and experienced specialists. Statistics suggest that the medical tourism industry in India is worth $333 million (Rs 1,450 Crore) while a study by CII-McKinsey estimates that the country could earn Rs 5,000-10,000 crore by 2012. The study predicts that, "by 2012, if medical tourism were to reach 25 per cent of revenues of private up-market players, up to Rs 10,000 Crore will be added to the revenues of these players". According to the Government of India, India's $17-billion-a-year health-care industry could grow 13 per cent in each of the next six years, boosted by medical tourism, which industry watchers say is growing at 30 per cent annually. Probably realizing the potential, major corporates such as the Tatas, Fortis, Max, Wockhardt, Piramal, and the Escorts group have made significant investments in setting up modern hospitals in major cities. Many have also designed special packages for patients, including airport pickups, visa assistance and board and lodging. The health care sector in India has witnessed an enormous growth in infrastructure in the private and voluntary sector. The private sector, which was very modest in the early stages, has now become a flourishing industry equipped with the most modern state-of-the-art technology at its disposal. It is estimated that 75-80% of health care services and investments in India are now provided by the private sector. An added plus had been that India has one of the largest pharmaceutical industries in the world. It is self-sufficient in drug production and exports drugs to more than 180 countries.

India has top-notch centres for open-heart surgery, pediatric heart surgery, hip and knee replacement, cosmetic surgery, dentistry, bone marrow transplants and cancer therapy, and virtually all of India’s clinics are equipped with the latest electronic and medical diagnostic equipment. Unlike many of its competitors in medical tourism, India also has the technological sophistication and infrastructure to maintain its market niche, and Indian pharmaceuticals meet the stringent requirements of the U.S. Food and Drug Administration. Additionally, India’s quality of care is up to American standards, and some Indian medical centres even provide services that are uncommon elsewhere. For example, hip surgery patients in India can opt for a hip-resurfacing procedure, in which damaged bone is scraped away and replaced with chrome alloy--an operation that costs less and causes less post-operative trauma than the traditional replacement procedure performed in the U.S.

While a large number of the private hospitals in India are willing to provide medical treatment to patients irrespective of nationality, only a few are in the forefront of promoting the health-hospitality mix. Some of the corporate hospitals in India that lead the medical tourism revolution are: i) Escorts Heart Institute & Research Centre, ii) Apollo Hospitals, iii) Wockhardt Hospitals, iv) Aravind Eye Hospitals, v) Fortis Healthcare, vi) Leelawati Hospital, vii) Dr. Vivek Saggar's Dental Care & Cure Centre, viii) NM Excellence, ix) Manipal Hospital, x) PD Hinduja National Hospital & Medical Research Centre, xi) LV Prasad Eye Institute, xii) B.M.Birla Herat Research Centre, xiii) Christian Medical College, iiv) Tata Memorial Cancer Hospital.

Apart from the private players, public sector hospitals like All India Institute of Medical Sciences (AIIMS) has been receiving patients from over 16 countries including European nations and there is a steady increase in the number of patients, mainly for complex surgical procedures. The AIIMS has also initiated a dedicated International Healthcare Service team, which will take care of the patient right from arrival till their departure coordinating all aspects of medical treatment.

Medical tourism: trends and prospects

Some of the key trends noted in the report on medical tourism published by TRAM (2006) include: i) Growing governmental intervention, ii) Growing international private sector investment and joint ventures, iii) Increasing supply of medical tourism products, leading to greater competition, iv) An increasing role for tourism suppliers in the packaging and marketing of medical tourism, v) Continuing barriers to medical tourism expansion, including lack of governmental agreements on payment for treatment abroad and insurance coverage, vi) Growing ethical concerns about medical tourism, which may limit growth in some regions. These trends are merely indicative and not comprehensive, nor do they take into account the nuances of individual country contexts.

There are definitely areas for improvement as the Indian healthcare industry starts marketing services to newer patient segments. A key difference in healthcare services in India, unlike the IT sector, is the critical role the government has to play to utilize medical tourism opportunity to its best. While responsible players have to be properly encouraged, quacks and overnight money swindlers have to be punished at the same time. Strict adherence to standards has to be ensured since the medical tourism product has the potential to be life threatening.

SWOT (Strengths, Weaknesses, Opportunities and Threats) (Table 1) analysis on the Indian medical tourism industry in its current state:

Table 1: Strengths, weaknesses, opportunities and threats.

|

Strengths

|

Weakness

|

|

· Quality Service at Affordable Cost

· Vast supply of qualified doctors

· Strong presence in advanced healthcare

e.g. cardiovascular, organ transplants–high success rate in operations

· International Reputation of hospitals and Doctors

· Diversity of tourism destinations and experiences

|

· No strong government support / initiative to promote medical tourism

· Low Coordination between the various players in the industry–airline operators, hotels and hospitals

· Customer Perception as an unhygienic country

· No proper accreditation and regulation system for hospitals

· Lack of uniform pricing policies across Hospitals

|

|

Opportunities

|

Threats

|

|

· Increased demand for healthcare services from countries with aging population (U.S, U.K)

· Fast-paced lifestyle increases demand for wellness tourism and alternative cures

· Shortage of supply in National Health Systems in countries like U.K, Canada

· Demand from countries with underdeveloped healthcare facilities

· Demand for retirement homes for elderly people especially Japanese

|

· Strong competition from countries like Thailand, Malaysia, Singapore

· Lack of international accreditation

· Overseas medical care not covered by insurance providers

· Under-investment in health infrastructure

|

Security threats for medical tourism industry in India

Patients from US/ UK and other developed countries are covered by insurance for ailments: People do not generally travel outside their normal place of stay for medical treatment unless there are compelling reasons. Since good quality care is available and the costs are taken care by insurance covers, patients from these regions do not travel to other destinations including India. Segments of customers who are either un-insured or under insured will travel for medical treatments. Also, customers will travel for medical procedures not covered by insurance.

Competition from neighboring countries especially Thailand and Singapore: The segments are different. While medical tourists visiting Thailand are primarily interested in combining their vacation with some medical procedure, India is receiving ‘mere patients’ who are less interested in leisure.

Lot of customers from non-English speaking countries: Prepare service providers and their employees for non-English linguist skills as more medical tourists from non-English speaking countries are expected

General infrastructure is not impressive: Health care system/ providers can do little about this. However they can offset part of discontent by showing concern and offering support service.

Visa related problems: i) Cost of medical visa is inhibitive. It is almost twice the cost of tourist visa, ii) It is not available in some countries from where India receives patients, iii) Some respondents have reported corruption in grant of visa (specifically complained), iv) Extension of visa takes time, v) Abuse of medical visa by tourists and accomplice, vi) A minimum two months cooling is required for re-entry on a medical visa which is restricted to three entries a year. For example, if a patient arrived for consultation, she/he must wait for at least two months to come back to India. It was told that India is losing these patients to Thailand, vii) Medical tourists travel on tourist visa which is cheaper and readily available, viii) Government should reassess the medical visa policy, ix) Should check corruption and facilitate medical visa.

Differential pricing: Some hospitals are using differential pricing for medical procedures. Whereas others have same prices for medical procedure but administer a different price for pre and post procedure care and arrangements. NRIs and PIO who are difficult to differentiate present self as domestic patients to avail lower prices. Similarly medical tourists from neighbouring countries also do not disclose their identity and seek price benefits posing as domestic patients.

There is no institutional tie-up: Indian hospitals with insurance companies in westerners/ developed world who are offering lower premium to their clients if they agree for a procedure in a low cost quality hospital at some other destination. There are such arrangements with hospitals especially in Singapore. This is going to be a big challenge for Indian medical tourism. Indian hospitals should aggressively seek such institutional tie-ups with insurance companies.

Recommendations to overcome the security threats

The Indian medical tourism industry can be world’s best medical tourism providing nation if it brings few changes in the style the government is running the industry. The hospitals in India are good but have to be upgraded to the international standards. The concept of luxury hospital should be implemented in this industry; which will give a better scope to grow further. The people in India should be taught how to behave with visitors through advertisements. Indian government should join hands with the private hospitals & provide them insurance facilities & technological help.

In local health care sector, the existing infrastructure is not sufficient to fulfill the needs of Indians, arrival of foreign patients would add more competition and difficulties. Star hospitals’ capacity is under-utilized, while public hospitals are overcrowded. Especially a technology based approach would hit common Indian hard as many of them cannot afford advanced technologies imported from the West. Why health care providers and governments of countries from where medical tourists hail would let their business go to their rivals? For instance, British government has already taken preventive measures by putting three hours flying limit for patients wishing to visit foreign medical destination. To become the leading medical tourism destination, India needs special infrastructure, good connectivity between principal cities, fast immigration process, accreditation of Indian hospitals and world class hospitals. Further, how the Indian government plans to handle cases of medical negligence as one bad case/incident draws undue flak from developed nations. What about post treatment/surgery issues after returning to homeland? Whether patients can afford to come again and again to India if needed? What about tourists suffering from contagious diseases? Estimates for medical tourism sector look very optimistic but to achieve them requires resources and serious commitment. All stakeholders have to ensure that foreign patients should not be given undue importance overlooking locals as it would set a bad precedent on the pretext of ‘Athithi Devo Bahav’.

Coding system

In India, the International Classification of Diseases (ICD) is being used in public health research as well as hospital information systems. However, morbidity and mortality coding is yet to be implemented in a uniform manner throughout India. A ‘National List of Diseases’, based on the ICD-10, is being used in hospitals through the Medical Certification of Cause of Death (MCCD) system for mortality coding and for morbidity statistics in some hospitals. Few instances of effective use of hospital data using the ICD coding systems for auditing clinical care are available from India. In the private sector, the ICD-10 is used mainly for medical coding and billing work for insurance purposes, and also as outsourced work by firms for clients in developed countries.

Where coding is done in hospital settings, the main problem seems to be inadequate training of practicing physicians and coders. The importance of writing up the cause-of-death report is not adequately emphasized and taught to medical practitioners. Most physicians ascribe the cause of death to the mechanism of death (eg. cardiorespiratory arrest) rather than the underlying cause of death. In other instances, faced with a situation of inadequate information in case records of patients, the physician writing the cause of death report tends to assign the death to the ‘unclassifiable’ category or to some miscellaneous codes. Poor maintenance of medical records also contributes to inaccurate assignment of the cause of death. However, this problem is not unique to India; it appears to be a problem in both developed and developing countries. While the problem is almost universal, the fact that it can be minimized has been shown through simple educational interventions aimed at medical students and residents.

The Ministries of Health, Home Affairs and Information Technology of the Government of India have identified the ICD-10 as the most suitable coding system for India compared with other system. The Directors of Health Services of all states/Union Territories have been advised to adopt the ICD-10 classification system for coding morbidity and mortality records. The Central Bureau of Health Intelligence (CBHI), the national nodal institution for health statistics in the Ministry of Health and Family Welfare, Government of India, has introduced an ‘Orientation training course on ICD-10’ to build capacity among officials engaged in preparation, handling and maintenance of health data. More such training programmes are needed to improve knowledge and skills in the fields of disease classification, coding and medical record-keeping and thereby improve the quality of health information generated by hospitals and surveys. Similar courses should be of benefit to health managers, hospital administrators, practicing physicians and medical coders. For medical coders, additional inputs on medical terminology, anatomy and physiology would also be required. Results of coding activities should be fed back to clinicians and coders for continuous improvement in quality. Technical support in information technology is also required for successful implementation of the health information system. In summary, recording and reporting systems need to be strengthened in India through human, financial and technological inputs for improved morbidity and mortality statistics, which are essential for evidence-based decision-making.

Patient care - Professional responsibility and liability

Medical tourism companies should be responsible for ensuring that their customers receive treatment that falls within the professional standard of care of the jurisdiction within which medical tourism agencies are located. Medical tourism companies should be prohibited from advertising and organizing treatment that is outside the professional standard of care and has not received federal approval by appropriate regulatory bodies in the countries within which medical tourism companies are located.

Restrictions must be placed upon the waiver of liability forms used by many medical tourism companies. These documents typically assert that customers of medical tourism companies cannot sue these businesses if patients are harmed while receiving care abroad. Clients of medical tourism companies should not be requested to waive their legal rights as a condition of establishing contracts with medical tourism agencies. Patients should retain the right to take legal action against medical tourism operators if patients are harmed as a result of receiving care in health-care facilities that lack international accreditation, if they are treated by health-care providers who are not licensed to provide medical care, if medical tourism companies make misleading or false claims about the effectiveness and safety of particular forms of care, and other circumstances in which patients make decisions on the basis of inaccurate, incomplete, false, or misleading information provided by medical tourism agencies. Medical tourism companies play a significant role in organizing cross-border health care. They need to be held accountable for their role in coordinating international health care. Defining responsibilities of medical tourism companies should help ensure that patients experience a high standard of care when they travel abroad for treatment.

To ensure that ‘medical tourists’ receive competent care abroad as well as proper follow-up care upon their return, medical tourism companies must be held to high standards of practice. Such an arrangement would differ from current circumstances, in which most medical tourism companies operate in a regulatory vacuum, use waiver of liability documents in an effort to avoid legal and financial responsibility when their customers receive negligent medical care or suffer serious post-operative complications and organize both medical services and travel arrangements while not being held to the standards of either health-care facilities or travel agencies. To protect patients engaging in cross-border health care, medical tourism companies must be held to demanding standards of practice. Quality in health care is often addressed in relation to hospitals, health-care systems and health-care professionals. As health care increasingly crosses national borders, efforts to improve quality in health care must also attend to the proliferation of medical tourism companies and the role of these businesses in promoting globalization of health services.

Challenges before medical tourism Industry

India is emerging as an attractive, affordable destination for healthcare but there are some challenges that the country has to overcome to become a tourist destination with competent health care industry:

Infrastructural facilities: i) Roads; ii) Sanitation; iii) Power Backups; iv) Rest/ Guest Houses; v) Public Utility Services.

The foreign customer concerns and expectations: The biggest challenge that the Indian hospitals face is assuring the foreign patients that they will receive quality care with no hidden costs. The industry experts need to develop the decision making models through a thorough study on the factors that motivate the patients to choose India as a health care solution spot. The basic expectations that the industry feels are important to be concerned about are: i) Hygiene; ii) Staff (trained technically as well as in soft skills); iii) Customization; iv) Insurance Cover; v) Stability; vi) Connectivity; vii) International standard certification.

The Image of India needs to be enhanced (Standardization): The only one quality that Indian health industry lacks in is health standards and hygiene. Indian hospitals lack accreditation from the Joint Commission on Accreditation of Healthcare Organisations (JCAHO), suffer from a lack of standards in terms of quality and rates for healthcare procedures, have no gradation system and a far from perfect insurance sector. In addition, top Indian hospitals have high infection and mortality rates, and are unwilling to disclose data regarding these.

Market accessibility: The next challenge for the Indian industry is to make the Indian market accessible by tourist travel agents and websites of Indian health tourism.The government can play a vital part as the same can bring in lots of foreign revenue. The major ways of promoting our health tourism could be: i) Tourist companies of India; ii) Doctors of India visiting foreign countries; iii) International websites on Indian tourism; iv) Globalisation of marketing activities by Indian travel agents; v) Tying up with foreign travel agents for promotion; vi) Insurance companies abroad who target customers.

Excess Glamourisation of Health Care: It has been seen that the doctors and key player hospitals in India emphasis more on glamorization of health care than its actual advantages or research uniqueness. We need to work ore on our research in medical field to be competent enough to beat our international competitor. In other words SERVICES should be given more attention and importance than PACKAGING.

State Intervention: As this is a product which needs international tie-ups and international marketing, the state should help in the same. It should help the companies, hospitals and states in promoting health tourism abroad so that we can tap a wider range of customers.

Infrastructure: Indian hospitals must create exclusive infrastructure for corporate medical tourism. Chartered flight services, attractive tourism packages could be part of infrastructure. There’s growing pressure on U.S. corporates to reduce expenditure on healthcare.

Competition (Neighboring countries): Countries that actively promote medical tourism include Cuba, Costa Rica, Hungary, India, Israel, Jordan, Lithuania, Malaysia and Thailand. Belgium, Poland and Singapore are now entering the field. South Africa specializes in medical safaris-visit the country for a safari, with a stopover for plastic surgery, a nose job and a chance to see lions and elephants. Thus India has enough competition from the international market. This will be one of our major threats in bringing up and developing the health tourism industry.

Insurance: Backup One good way of tapping the foreign customers is tying up with Insurance companies broad who could provide a genuine database of target customers. They can benefit from us by our services. Thus this would become a way of mutual marketing tactics between the Indian health tourism industry and the foreign Insurance agencies.

Local Demand vs Global Demand: It can be seen in case of hospitals like Apollo and Escorts that the Local demand itself to be catered to is vast. We should remember that we should have the facilities enough to manage the foreign customers not neglecting the local markets. Thus it is a challenge for both the Alternate therapy industry and Corporate Health Care Service Providers to cater to this vast market efficiently without compromises in quality on either side.

Recommendations

The promoters should concentrate more on publicity of medical tourism as the awareness about medical tourism among people is very low. The heath care centers can also dispatch membership card to their customers, this will result in retaining of the customers for a longer period of time. The promoters can encourage the tourists to recommend their health care centers to others as mouth to mouth information is effective and does not any money. The promoters should ensure that they cover all kinds of health insurance provided in different nations, and encourage customers to take up health insurance, as this will simplify the transaction process. The promoters should hold various campaigns in different nations and continents and offer better discount packages.

Suggestions for developing Indian medical tourism

The following suggestions lay down the future path for India to achieve leadership position in medical tourism. These suggestions largely draw from the discussions with various stakeholders as well as observing the other countries’ medical tourism conditions: i) Role of Government, ii) Medical Visas, iii) Holistic medical and diagnostic centers within the corporate hospitals, iv) Setting up national level bodies, v) Integrate vertically, vi) Joint ventures/ alliances.

Conflict of interest

The authors declare no conflict of interest.

References

1. Baru RV. Privatisation and Corporatisation, Seminar, 2000; 489:29–22.

2. Bookman, M. & Bookman, K. “Medical Tourism in Developing Countries “, New York : Palgrave Macmillan 2007.

3. Carrera PM, Bridges JFP Globalisation and Healthcare: Understanding Health and Medical Tourism, Expert review of Pharmaco economics and Outcomes Research 2006; 6(4):447–454.

4. Chartered Institute of Marketing. Marketing and the 7Ps A brief summary of marketing and how it works 2005. (Accessed on March 1, 2008: www.cim.co.uk/MediaStore/FactFiles/Factifile7ps.pdf).

5. CII-McKinsey. “Health Care in India: The Road Ahead”, CII, McKinsey and Company and Indian Healthcare Federation, New Delhi, 2002.

6. Connell J. Medical Tourism: Sea, Sun, Sand and Surgery”, Tourism Management, 2006; 27(6):1093–1100.

7. Dogra, Sapna. Can Delhi Be a Successful Mode l for Medical Tourism? Express, 2003.

8. Healthcare Management, 1-15 September. (Accessed on 21 January 2008: http://www. expresshealthcaremgmt.com/20030915/focus01).

9. Kaur J, Sundar GH, Vaidya D, Bhargava S. Health Tourism in India - Growth and Opportunities. Proceedings, International Marketing Conference on Marketing & Society, 415-422. (Accessed on 2 September 2007: http://dspace.iimk.ac.in/bitstream/2259/345/1/415-422.pdf.

10. Kohli, Shweta Rajpal. Medical Tourism Growing at 30% a Year: Study 2002; (Accessed 27 November 2009: http:// www.rediff.com/money/2002/nov/12med.htm).

11. Mathers CD, Murray CJ, Ezzati M, Gakidou E, Salomon JA, et al. Population health metrics: Crucial inputs to the development of evidence for health policy. Popul Health Metr. 2003; 1:6.

12. World Health Organization. History of the development of ICD. (accessed on 20 August 2005: http://www.who.int/classifications/icd/en/HistoryOfICD.pdf.

13. World Health Organization. International Statistical Classification of Diseases and Related Health Problems. 10th revision. Current version. Version for 2003. (Accessed on 8 March 2005: http://www.who.int/classifications/icd/en/).

14. Central Bureau of Health Intelligence. Module and workbook: Orientation training on ICD-10. New Delhi: Directorate General of Health Services, Ministry of Health and Family Welfare, Nirman Bhavan. (Accessed on 15 June 2005: www.cbhidghs.nic.in).

15. Lopez AD, Mathers CD, Ezzati M, Jamison DT, Murray CJL (eds). Global burden of disease and risk factors. New York: Oxford University Press; 2006.

16. The World Bank. Disease control priorities project. New York: Oxford University Press; 2006. (accessed on 15 October 2006: at http://www.dcp2.org/main/Home.html.

17. Gajalakshmi V, Peto R, Kanaka S, Balasubramanian S. Verbal autopsy of 48000 adult deaths attributable to medical causes in Chennai (formerly Madras), India. BMC Public Health 2002; 2:7.

18. Joshi R, Cardona M, Iyengar S, Sukumar A, Raju CR, et al. Chronic diseases now a leading cause of death in rural India—mortality data from the Andhra Pradesh Rural Health Initiative. Int J Epidemiol. 2006; 35:1522–1529.

19. Registrar General, India. Maternal mortality in India: 1997–2003. Trends, causes and risk factors. New Delhi: (Accessed on 22 December 2006: www. censusindia.net/Maternal_Mortality_in_India_1997–2003.

20. Jha P, Gajalakshmi V, Gupta PC, Kumar R, Mony P, et al. RGI–CGHR Prospective Study Collaborators. Prospective study of one million deaths in India: Rationale, design, and validation results. PLoS Med. 2006; 3:e18.